)

Has the AI sell-off made cybersecurity more compelling?

- Wealth

- Management

Hugh Lam

)

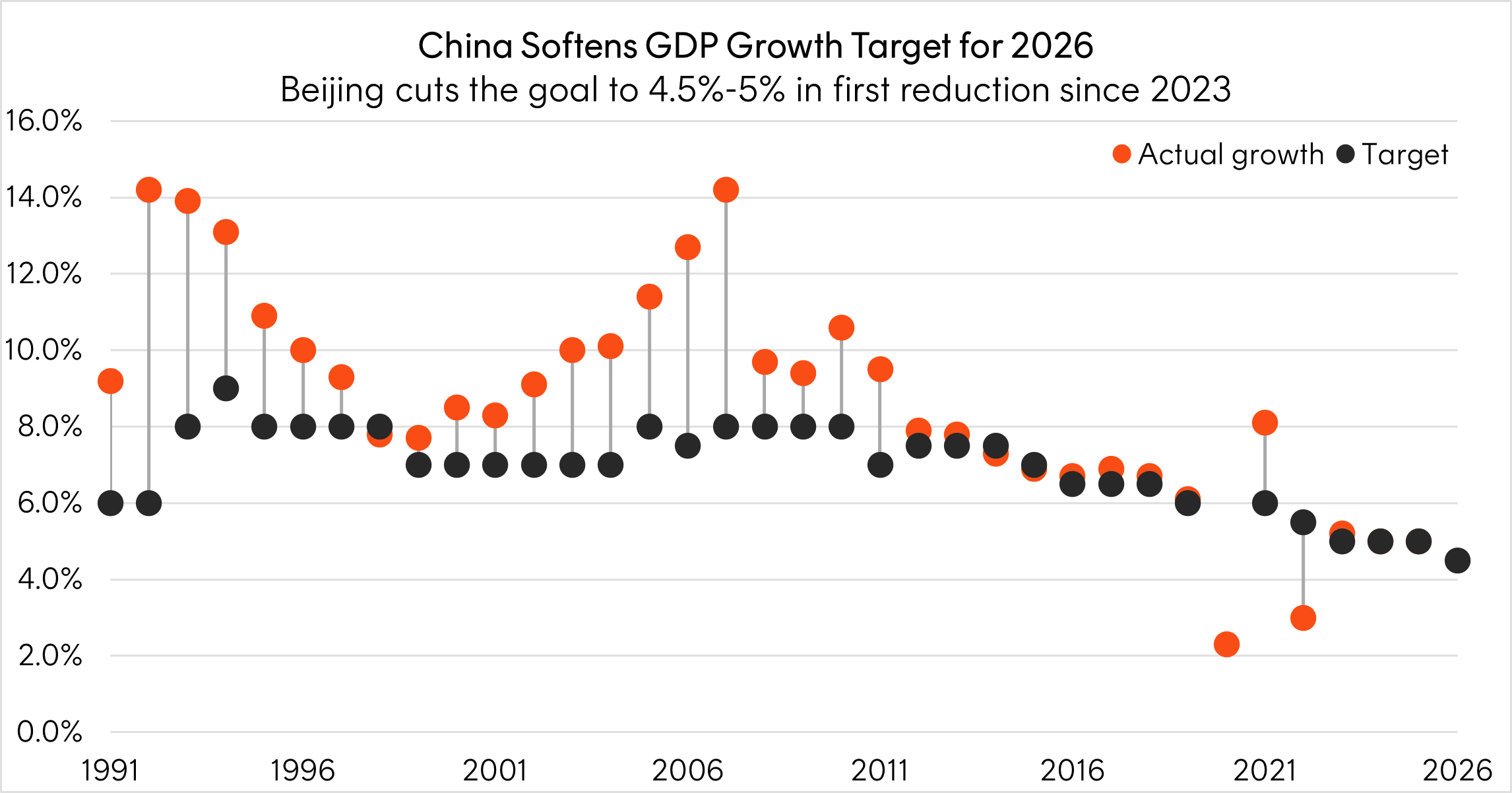

Each year, China’s National People’s Congress (NPC) and its political advisory body, the CPPCC, convene for what is known as the ‘Two Sessions’ meeting. Closely watched by investors around the world, it provides a rare and direct window into Beijing’s thinking on the economy with the country’s GDP growth target, fiscal priorities, and key policy agenda set for the year ahead.

In the following section, we look at key similarities and differences between the Two Sessions meeting this year and last year:

1. The most notable shift was the GDP target moving from a single figure of ‘around 5%’ to a range of 4.5–5%, signalling a deliberate move away from ‘growth at any cost’ toward prioritising high quality, sustainable development. While the softer target may be viewed negatively, the range provides more policy flexibility with room to either meet the minimum target or to surprise on the upside. Ultimately, the change reflects an acknowledgment from the Chinese government that the external trade environment remains highly uncertain and that recalibrating internal growth drivers away from exports toward consumption will take some time.

Source: National Bureau of Statistics, annual government work reports, Bloomberg. Note: China didn’t set an annual growth target for 2020, when the pandemic first hit. Figures represent the lower bound when targets are set as a range.

Source: National Bureau of Statistics, annual government work reports, Bloomberg. Note: China didn’t set an annual growth target for 2020, when the pandemic first hit. Figures represent the lower bound when targets are set as a range.

2. That said, the scale of fiscal policy support largely remains the same with the deficit-to-GDP ratio target, local government special-purpose bonds and ultra-long special treasury bonds issuance amounts unchanged. However, bank recapitalisation bonds fell from 500bn yuan (2025) to 300bn yuan (2026), and the consumer trade-in program allocation fell modestly from 300bn yuan to 250bn yuan – likely an acknowledgement that the direct subsidies may have a ceiling in terms of their ability to materially shift consumer spending patterns in a population that is structurally inclined to save.

3. Positively, self-sufficiency in strategically important industries such as in science and technology remain a key priority for the government. The AI Plus Initiative will expand to build AI technologies from the ground up whether that be through the development of AI agents, open-source AI communities and AI native business models. New infrastructure projects on hyper-scale intelligent computing clusters and electricity supply will also be launched.

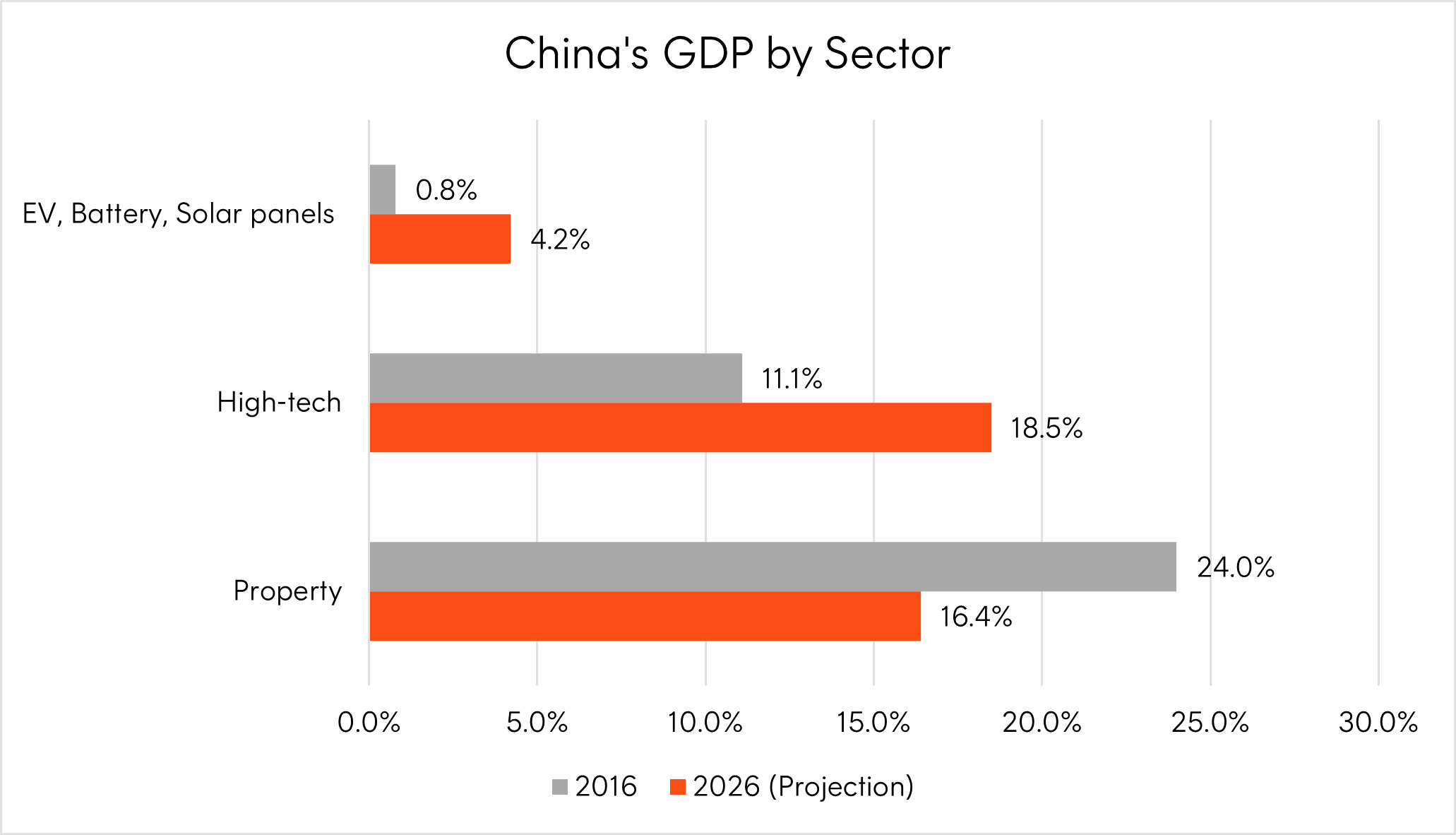

Source: Bloomberg Economics. As at 2024. Actual outcomes may vary.

Source: Bloomberg Economics. As at 2024. Actual outcomes may vary.

Perhaps the most significant and underappreciated aspect of this year’s Two Sessions is that the 2026 Government Work Report contains a new section presenting the 15th Five-Year Plan outline for 2026–2030. Some of the key targets include:

R&D spending to grow at least 7% annually — sustaining the innovation investment trajectory of the 14th FYP period

Digital economy core industries to reach 12.5% of GDP — up from ~10.5% today, representing a substantial structural shift in the economy’s composition

Total CO₂ intensity reduction of 17% over the plan period — creating a durable, multi-year policy tailwind for clean energy and green technology

109 major projects across six areas, including 28 focused on new quality productive forces, 23 on new infrastructure, and 18 on the green and low-carbon transition.

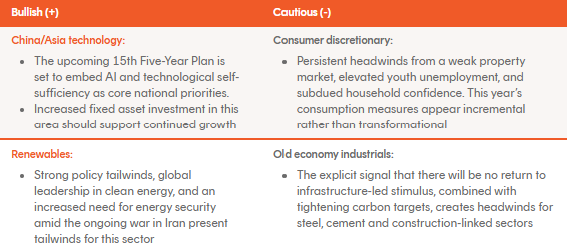

All in all, the 2026 Two Sessions reinforces a selective rather than broad approach to Chinese equities. In our view, the policy mix increasingly rewards sectors tied to the innovation, self-sufficiency and clean energy themes – while penalising sectors reliant on infrastructure spending or consumer confidence that has yet to meaningfully recover.

Of course, ongoing developments in Iran remain a left tail risk for China from an energy supply perspective with sustained higher oil prices a net drag on economic growth. That said, China can replace lost volumes by increasing imports from other parts of the world like Saudi Arabia, Russia and Brazil.

The following is a summary of our key views within the China equity market:

Published with permission - Betashares Holdings Pty Ltd.

Source: Betashares

Betashares Capital Ltd (ABN 78 139 566 868 AFSL 341181) (Betashares) is the responsible entity and issuer of the Betashares Funds, as well as Betashares Invest, the IDPS-like scheme available through Betashares Direct. Bendigo Superannuation Pty Ltd (ABN 23 644 620 128 AFSL 534006) (Bendigo Super) is the trustee of the Bendigo Superannuation Plan (ABN 57 526 653 420), which includes the Bendigo SmartStart Super and Bendigo SmartStart Pension (Super Products).

Before making an investment decision, read the relevant Product Disclosure Statement (PDS), available at: (i) www.betashares.com.au or by calling 1300 487 577 for the Betashares Funds, (ii) www.betashares.com.au/super or by calling 1800 033 426 for the Super Products, and (iii) www.betashares.com.au/direct for Betashares Invest. You can also obtain a copy of any Betashares disclosure document by emailing Customer Support at support@betashares.com.au.

You may also wish to consider the relevant Target Market Determination, which sets out the class of consumers that comprise the target market for the relevant Betashares product, available: (i) at www.betashares.com.au/target-market-determinations for the Betashares Funds, (ii) here for Bendigo SmartStart Super Target Market Determination and here for Bendigo SmartStart Pension, and (iii) at www.betashares.com.au/direct for Betashares Invest.

Investments in the Betashares products are subject to investment risk and the value of units may go up and down. The performance of any Betashares product is not guaranteed by Betashares, Bendigo Super or any other person.

This information is general in nature and doesn’t take into account any person’s financial objectives, situation or needs. You should consider its appropriateness taking into account such factors and seek professional financial advice.

)

)

)

)

Our boutique size enables Specialised Private Capital to forge relationships with well regarded investment firms.

Contact UsKeep up with the latest news and insights at Specialised Private Capital Ltd